안녕하세요, 한양세무회계사무소 조규섭 사무장입니다.

다주택자의 경우 대부분 임대소득이 발생하고 있을텐데, 임대료 외에 간주임대료 부분도 고려를 해서 임대소득을 계산해서 임대소득에 대한 과세에 대비를 해야 합니다.

오늘은 임대소득에 대해서 전반적으로 알아보겠습니다.

먼저, 주택수에 따라 달라지는 과세 원칙입니다.

소유주택에 따른 과세·비과세

① 임대료/간주임대료 계산

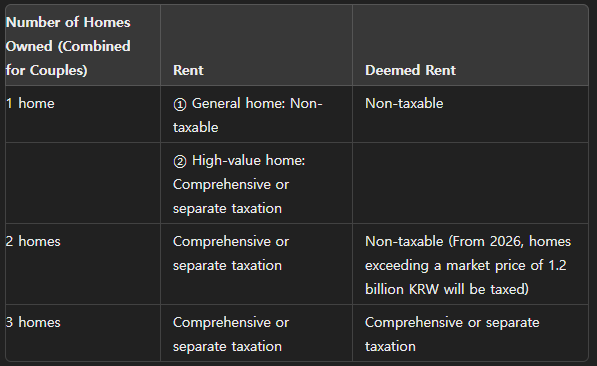

거주자가 3주택이상이 되는 경우 간주임대료가 과세됩니다. 기본적으로 임대소득이 2천만원 이하인 경우에는 종합소득세(6~45%)에 포함되지 않고 분리과세(14%)로 끝나게 되는데요, 주택에 따른 임대료/간주임대료 계산은 아래와 같습니다.

| 주택 소유(부부합산) | 임대료 | 간주임대료 |

| 1주택 | ① 일반주택 : 비과세 ② 고가주택 : 종합과세 또는 분리과세 |

비과세 |

| 2주택 | 종합과세 또는 분리과세 | 비과세 (2026년부터 기준시가 12억 초과 2주택은 과세) |

| 3주택 | 종합과세 또는 분리과세 | 종합과세 또는 분리과세 |

② 공동소유 주택의 주택수 계산

공동소유 주택은 원칙적으로 최다지분자의 소유주택으로 계산을 하지만, 세법개정으로 2020년 귀속부터는 소수지분자의 주택수에도 포함되기도 합니다.

ⓐ 해당 주택에서 발생하는 임대소득 수입금액(주택의 총 임대수입금액 × 지분율)이 연간 600만원 이상인 경우

ⓑ 기준시가가 12억원을 초과하는 주택의 30%를 초과하는 공동지분을 소유(기준시가 12억원과 지분율 30%는 과기간 말일 또는 양도일 기준으로 판단)인 경우

부부의 경우도 살펴봅시다. 본인과 배우자가 각각 주택의 소유한 경우에 부부합산하여 주택 수를 계산하지만, 동일 주택이 부부 각각의 주택수에 추가된 경우에는 아래와 같이 판단해서 1인 소유주택으로 계산할 수 있습니다.

ⓐ 부부 중 지분이 더 큰 자의 주택수로 먼저 계산합니다.

ⓑ 2지분이 동일한 경우, 부부사이의 합의에 따라 소유주택에 가산하기로 한 자로 주택수를 계산합니다.

주택임대소득 분리과세 계산구조 - 종합과세/분리과세 선택 확인

일단 임대소득이 2천만원 이하인 경우를 고려해보겠습니다. 2천만원 이상이면 그냥 종합소득세 합산과세라서 종합소득세를 내시면 됩니다.

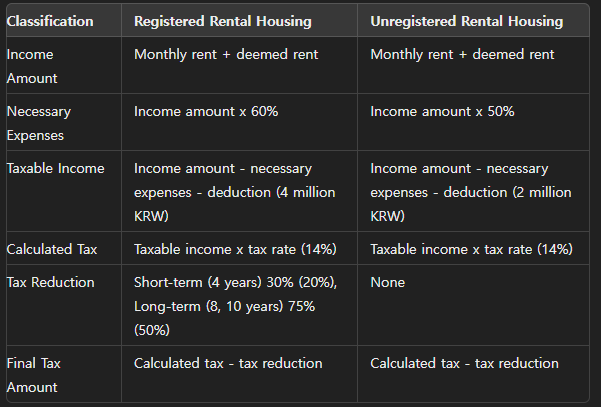

| 구분 | 등록임대주택 | 미등록임대주택 |

| 수입금액 | 월세 + 간주임대료 | 월세 + 간주임대료 |

| 필요경비 | 수입금액 x 60% | 수입금액 x 50% |

| 소득금액(과세표준) | 수입금액 - 필요경비 - 공제금액(4백만원) | 수입금액 - 필요경비 - 공제금액(2백만원) |

| 산출세액 | 과세표준 x 세율(14%) | 과세표준 x 세율(14%) |

| 세액감면 | 단기(4년) 30%(20%), 장기(8,10년) 75%(50%) | 없음 |

| 결정세액 | 산출세액 - 세액감면 | 산출세액 - 세액감면 |

* 등록임대주택 : 지자체와 세무서에 모두 등록하고 임대료의 증가율이 5%를 초과하지 않아야 함

* 공제금액 : 분리과세 주택임대소득을 제외한 종합소득금액이 2천만원 이하인 경우 4백만원(등록) 또는 2백만원(미등록) 공제

* 세액감면 : 국민주택규모 주택으로 「조세특례제한법」 제96조의 요건을 충족하여야 함

* (’20.8.18.) 「민간임대주택에 관한 특별법」 개정으로 단기임대 및 아파트 장기임대 폐지, 10년 장기임대 신설

등록임대주택은 아무래도 장기적으로 임대사업을 하려고 하시는 분들의 경우이고, 이에 대한 장기보유 및 임대소득에 대한 세액감면의 혜택이 있으나 매도가 자유롭지 않아서 좀 꺼려하는 부분이 있습니다.

하지만 임대소득에 대한 세금만 본다면 등록임대주택으로 가는게 낫겠죠?

위와 같이 종합과세와 분리과세는 복잡하지만, 종합과세/분리과세를 선택하는 것에 따라 세금이 달라질 수 있으니 종합소득세 신고시즌에는 항상 고민을 해보셔야 합니다.

종합과세의 낮은 세율은 6%, 15%이기 때문에 거의 대부분은 분리과세가 낫지만 6%구간대의 종합과세가 나오는 임대소득자들은 그걸 고려해볼 수 있겠죠.

사업자 등록에 따른 세금 혜택을 확인하세요

「소득세법」에 따른 사업자등록과 「민간임대주택에 관한 특별법」에 따른 임대사업자등록을 모두 하고 일정 요건을 충족하는 경우 분리과세 필요경비율과 공제금액에 혜택이 있으며, 소형주택 임대사업자에 대한 세액감면을 받을 수 있습니다

ⓐ 필요경비율 : 미등록 50%→등록 60%

ⓑ 공제금액 : 미등록 2백만원→등록 4백만원

ⓒ 감면율 : 감면대상 소득세의 30%(2호 이상 임대 시 20%), 장기일반민간임대주택 등은 75%(2호 이상 임대 시 50%)

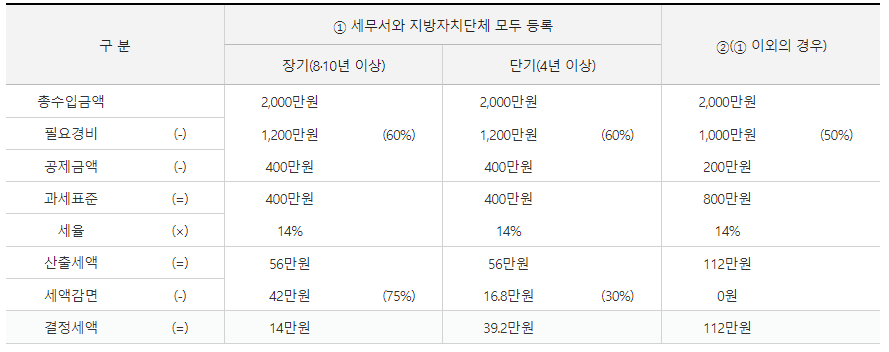

가정】

주택임대소득 외의 다른 종합소득금액은 2천만원 이하

①은 세무서와 지방자치단체 모두 등록한 경우로서 필요경비 및 공제금액 혜택요건과 감면요건 충족

⇒ 사업자등록 등 우대요건을 충족한 경우 결정세액은 14만원(장기), 39.2만원(단기)으로 등록하지 않은 경우 112만원 보다 유리(소득세만 비교한 결과임)

다만, 감면 등을 받은 후에 의무임대기간을 준수하지 않은 경우에는 감면 세액과 이자상당액을 추징 당할 수 있습니다.

그렇기 때문에 본격적인 임대사업을 할 것인지에 따른 고민이 필요합니다.

소득세를 미리 신고·납부하세요.

소득세를 신고·납부하지 않거나 과소신고·납부한 것으로 확인되면 가산세를 추가로 부담할 수 있습니다.

미리 납부하는 것. 이것도 절세의 비법입니다.

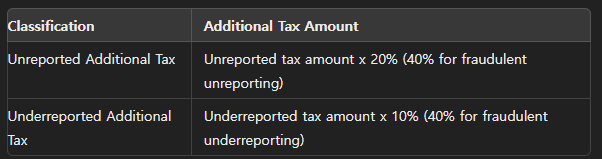

| 구분 | 가산세액 |

| 무신고 가산세 | 무신고 납부세액 × 20%(부정무신고는 40%) * 복식부기의무자는 위 금액과 수입금액의 0.07% (부정무신고는 0.14%)와 비교해서 큰 금액 |

| 과소신고 가산세 | 과소신고 납부세액 × 10%(부정과소신고는 40%) * 복식부기의무자가 부정과소신고한 경우 위 금액과 수입금액의 0.14%와 비교해서 큰 금액) |

| 납부지연 가산세 | 무・과소납부 세액 × 납부지연 일수 × (22/100,000) |

세금고민, 함께 나누세요

세금은 항상 고민하는 만큼 절세할 수 있습니다.

한양세무회계사무소는 항상 열려 있습니다.

언제든 편하게 고민을 털어놓을 수 있는 그런 세금 파트너이기 때문에, 부담없이 연락주세요 ㅎㅎ

언제나 에너지 넘치게 세상 모든 세금 걱정을 함께 하는 한양세무회계사무소가 되겠습니다.

더욱 더 화이팅!!

연락하실 곳

사무실 : 055-292-7760

김상옥 세무사 : 010-2590-7760

조규섭 사무장 : 010-3020-4815 (주말 상담가능)

Hello, I am Jo Gyu-seop, an office manager at Hanyang Tax & Accounting Office. For multi-homeowners, rental income is usually generated, and in addition to rental fees, deemed rent should also be considered when calculating rental income to prepare for taxation on that income.

Today, let's take a comprehensive look at rental income.

Taxation Principles Depending on the Number of Homes Owned

Taxation and Non-Taxation Based on Home Ownership

1. Calculation of Rent/Deemed Rent

When a resident owns three or more homes, deemed rent is taxable. If the rental income is 20 million KRW or less, it is not included in the comprehensive income tax (6-45%) and is subject to separate taxation (14%). The calculation of rent and deemed rent based on the number of homes is as follows:

2. Calculating the Number of Homes for Co-owned Properties

As a general rule, co-owned properties are calculated based on the home owned by the person with the largest share. However, from 2020, due to tax law changes, properties may also be included in the home count for those with smaller shares if:

- The rental income from the property (total rental income from the property × share ratio) is 6 million KRW or more per year.

- The market price of the home exceeds 1.2 billion KRW and the ownership share is more than 30% (assessed based on the end-of-term or sale date).

Let's also consider the case for married couples. When both a person and their spouse own homes, the number of homes is calculated on a combined basis. However, if the same home is counted for both spouses, it can be calculated as a single-owner home as follows:

- The home is first calculated as owned by the person with the larger share.

- If the shares are equal, the calculation is based on an agreement between the couple on which person to count the home for.

Separate Taxation Structure for Rental Income - Determining Whether to Choose Comprehensive or Separate Taxation

Let's consider cases where rental income is 20 million KRW or less. If it exceeds 20 million KRW, it is simply added to comprehensive income and taxed as such.

* Registered rental housing must be registered with both the local government and tax office, and rent increase must not exceed 5%.

* Deduction: If the combined comprehensive income excluding separately taxed rental income is 20 million KRW or less, a deduction of 4 million KRW (registered) or 2 million KRW (unregistered) is applied.

* Tax Reduction: To be eligible for the tax reduction for homes of a certain size, the conditions outlined in Article 96 of the "Special Tax Treatment Control Act" must be met.

* As of August 18, 2020, the "Special Act on Private Rental Housing" has been amended to abolish short-term rental and long-term apartment rental and establish a 10-year long-term rental.

Registered rental housing is generally for those who intend to engage in long-term rental business. There are benefits such as long-term holding and tax reductions on rental income, but the reluctance comes from the lack of freedom to sell. However, if we only consider the tax on rental income, registering as a rental property would be more advantageous.

As you can see, whether you choose comprehensive or separate taxation can make a big difference in the tax amount. Therefore, it's always worth considering during the comprehensive income tax filing season. While comprehensive taxation has a low rate of 6% or 15%, in most cases, separate taxation is more advantageous. However, for those whose rental income falls in the 6% bracket, comprehensive taxation might be worth considering.

Confirm the Tax Benefits of Business Registration

If you register as a business under the "Income Tax Act" and as a rental business under the "Special Act on Private Rental Housing" and meet certain requirements, there are benefits for the necessary expense rate and deduction amount in separate taxation, as well as tax reductions for small rental housing businesses.

- Necessary Expense Rate: 50% for unregistered → 60% for registered

- Deduction Amount: 2 million KRW for unregistered → 4 million KRW for registered

- Reduction Rate: 30% of the tax reduction target income tax (20% for 2 or more rentals), 75% for long-term general private rental housing, etc. (50% for 2 or more rentals)

For example, if the other comprehensive income besides rental income is 20 million KRW or less, and you have met all the requirements for both tax office and local government registration:

- The determined tax amount would be 140,000 KRW (long-term) and 392,000 KRW (short-term), which is more advantageous than the 1.12 million KRW when not registered (comparison based solely on income tax).

However, if the tax benefits are taken and the mandatory rental period is not complied with, you may be subject to the recovery of the reduced tax amount and interest. Therefore, it's important to carefully consider whether to engage in a full-scale rental business.

Report and Pay Income Tax in Advance

If income tax is not reported or paid, or if it is underreported or underpaid, additional penalties may be incurred.

Paying in advance can also be a way to save on taxes.

* For those obligated to keep double-entry bookkeeping, compare the above amount with 0.07% of the income amount (0.14% for fraudulent unreporting) and use the larger amount.

* For underreported tax by those obligated to keep double-entry bookkeeping, compare the above amount with 0.14% of the income amount (for fraudulent underreporting) and use the larger amount.

* For delayed payment additional tax, the formula is: unpaid or underpaid tax amount x days delayed x (22/100,000)

Share Your Tax Concerns

The more you think about taxes, the more you can save.

Hanyang Tax & Accounting Office is always open. We are your tax partner who you can always reach out to comfortably, so feel free to contact us.

We will continue to work energetically to solve all your tax worries together!

Keep fighting!

Contact Information

Office: 055-292-7760

Tax Accountant Kim Sang-ok: 010-2590-7760

Office Manager Jo Gyu-seop: 010-3020-4815 (Weekend consultations available)

'세금이야기 > 소득세' 카테고리의 다른 글

| 11월은 개인사업자 중간예납의 시즌입니다 _ 한양세무회계사무소 (12) | 2024.11.09 |

|---|---|

| 사업용카드의 오해와 진실_한양세무회계사무소 [창원세무사/김해세무사] (8) | 2024.09.11 |

| 9월 19일까지 2024년 상반기 근로장려금 신청하세요_한양세무회계사무소 [창원세무사/김해세무사] (16) | 2024.09.04 |

| 민간 업체? NO! NO! 국세청이 직접 소득세 환급금을 찾아드립니다_한양세무회계사무소 [창원세무사/김해세무사] (3) | 2024.08.29 |

| 사업을 시작하면 장부기장을 맡기세요_한양세무회계사무소 [창원세무사/김해세무사] (0) | 2024.08.28 |

댓글